The STOCK Act is defined as the Stop Trading on Congressional Knowledge Act, a federal law signed on April 4, 2012 that prohibits members of Congress and federal employees from trading stocks based on material nonpublic information (MNPI) obtained through their official positions. Before this law, a legal gray area allowed lawmakers to trade freely on sensitive government information without consequence. The STOCK Act closed that gap by confirming that insider trading laws apply to Congress, and by requiring public disclosure of trades above a set threshold. Understanding what this law does, and where it falls short, matters for every investor who follows congressional trading activity.

What is the STOCK Act explained: core definition and purpose

The STOCK Act does two distinct things. It creates mandatory disclosure rules for congressional stock trades, and it affirms insider trading prohibitions legally apply to members of Congress. That second point is more significant than most people realize. Before 2012, Congress had never explicitly been bound by the same securities laws that govern corporate executives. The Act changed that in writing.

The law covers members of the House and Senate, their staff, and a broad range of executive branch employees. It targets trades made using MNPI, which means information not available to the general public that would likely affect a stock's price if it were released. Think of a senator on the Armed Services Committee learning about a classified defense contract before it is publicly announced, then buying shares in the winning contractor. That is exactly the behavior the STOCK Act targets.

The law also established Periodic Transaction Reports (PTRs) as the primary transparency mechanism. These are public filings that document when a covered official buys or sells a qualifying financial asset. PTRs are accessible online, and watchdog organizations, financial platforms, and journalists use them to track congressional trading patterns.

What Congress must disclose under the STOCK Act

The disclosure rules are specific. Covered transactions over $1,000 must be reported within 45 days of the trade date via a Periodic Transaction Report. That 45-day window is the outer limit, not a target. Some members file within days; others push right to the deadline or beyond it.

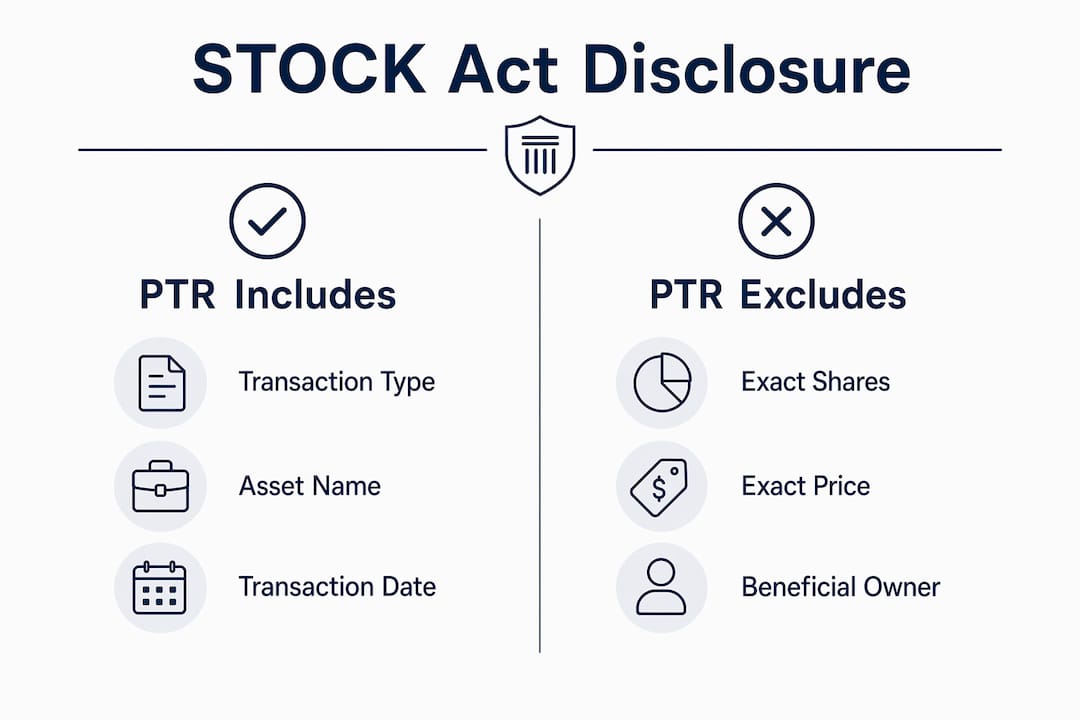

Each PTR must include:

- Transaction type: Buy, sell, or exchange

- Asset name: The stock, bond, or fund involved

- Transaction date: When the trade was executed

- Dollar value range: Reported in bands (e.g., $1,001 to $15,000; $15,001 to $50,000)

What PTRs do not include is equally important. Disclosures omit exact share counts and exact execution prices. They report value in ranges, not precise figures. They also provide no explanation of why the trade was made. A senator selling $50,000 in pharmaceutical stock the week before a drug approval decision looks suspicious on paper, but the PTR itself tells you nothing about intent.

| PTR includes | PTR does not include |

|---|---|

| Transaction type (buy/sell) | Exact number of shares |

| Asset name and ticker | Exact execution price |

| Transaction date | Reason for the trade |

| Dollar value range | Whether MNPI was used |

This distinction matters. PTRs are transparency tools, not evidence of wrongdoing. Treating every congressional trade as proof of insider trading misreads what the disclosure actually shows.

The gap between trade date and filing date can stretch the full 45 days, meaning public data may already be stale by the time you see it. A trade made on January 1st might not appear in public records until February 15th. For investors trying to mirror congressional trades in real time, this delay is a serious limitation.

Pro Tip: When reading a PTR, always check both the transaction date and the filing date. A wide gap between the two can signal a pattern of late disclosure worth noting.

How the STOCK Act extends insider trading law to Congress

The legal foundation of the STOCK Act sits in 15 U.S.C. § 78u-1(g), which establishes a statutory duty of trust and confidence for members of Congress. This is the legal mechanism that makes congressional insider trading prosecutable under the same securities laws that apply to corporate executives.

Before the STOCK Act, prosecutors faced a real problem. Traditional insider trading law required proving a fiduciary duty between the trader and the source of the information. Corporate insiders owe clear fiduciary duties to their companies and shareholders. Members of Congress owe duties to their constituents and the public, which is a much harder legal relationship to define in securities law terms. The STOCK Act resolved this by codifying the duty directly in statute.

That said, practical enforcement still faces significant barriers. The Speech or Debate Clause of the U.S. Constitution protects lawmakers from legal liability for official legislative acts. Prosecutors must prove that a specific trade was made using specific nonpublic information obtained through an official position. That causal chain is difficult to establish in any insider trading case, and congressional cases add constitutional complexity on top of the standard evidentiary challenges.

Key legal distinctions between congressional and corporate insider trading:

- Corporate insiders have clear, defined fiduciary duties to shareholders

- Congressional members have a statutory duty created by the STOCK Act itself

- Corporate insider trades are monitored by the SEC with established enforcement protocols

- Congressional trades are disclosed publicly but enforcement falls to ethics committees with limited power

- Proving MNPI use in congressional trades requires establishing both the duty and the causal link to the trade

Pro Tip: The STOCK Act creates legal liability in theory. Whether that liability is ever enforced is a separate question entirely, and the track record so far is not encouraging.

What enforcement looks like under the STOCK Act

The enforcement reality of the STOCK Act is blunt. The maximum penalty for a late disclosure is $200, and that fine is frequently waived. For a member of Congress earning $174,000 per year and potentially trading far larger sums, a $200 fine is not a deterrent. It is barely an inconvenience.

More striking is this: no member of Congress has ever been prosecuted under the STOCK Act since it became law in 2012. Late filings are common. Trades that appear to coincide with nonpublic legislative activity have been documented by journalists and watchdog groups. Yet the Act's enforcement mechanisms have never produced a criminal case.

"The STOCK Act has never produced a single prosecution despite overwhelming evidence of insider trading patterns and frequent late filings." — Riptide Report, 2026

Enforcement responsibility is split between the House and Senate ethics committees and the Department of Justice. Ethics committees have historically been reluctant to investigate their own members aggressively. The DOJ can pursue criminal insider trading charges under general securities law, but the evidentiary bar is high and constitutional protections add friction.

The contrast with SEC enforcement of corporate insider trading is sharp. The SEC has dedicated surveillance systems, subpoena power, and a track record of civil and criminal referrals. Congressional oversight of its own members has none of those structural advantages. Understanding this gap is central to any honest stock act summary.

Practical implications for investors and public transparency

For retail investors, the STOCK Act's most practical output is the public PTR database. Organizations like Signal Congress and Congressional Trader parse these filings and present them in readable formats. Ai-stockscout also tracks congressional trade data as part of its alternative data suite, giving users a real-time view of what lawmakers are buying and selling.

The key misconception to avoid is treating PTR data as a trading signal with an edge. Disclosures show transaction occurrence and basic details, but they cannot prove intent or insider trading by themselves. A senator buying Apple stock tells you nothing about whether that purchase was based on privileged information or a routine portfolio rebalance. The data is useful for pattern recognition and public accountability, not for direct trade replication.

Ongoing legislative efforts reflect growing frustration with the current framework. Bills like the ETHICS Act and the Ban Stock Trading for Government Officials Act have been proposed in recent sessions to prohibit members of Congress from trading individual stocks entirely. None have passed as of 2026, but the political pressure is building.

How investors and analysts actually use STOCK Act data:

- Watchdog monitoring: Tracking patterns of trades that precede major legislative votes or regulatory announcements

- Sector signals: Identifying which industries attract the most congressional buying or selling during specific policy cycles

- Accountability journalism: Documenting late filers and repeat offenders for public scrutiny

- Alternative data feeds: Platforms that aggregate PTR filings alongside other signals like dark pool activity and social sentiment

Pro Tip: Use congressional trade data as one signal among many, not as a standalone strategy. Combine it with earnings calendars, sector news, and technical levels for a fuller picture.

Key takeaways

The STOCK Act requires transparency and establishes legal liability for congressional insider trading, but weak enforcement penalties and zero prosecutions since 2012 mean the law's deterrent effect remains largely theoretical.

| Point | Details |

|---|---|

| Core definition | The STOCK Act prohibits Congress from trading on MNPI and requires public disclosure of qualifying trades. |

| Disclosure window | Trades over $1,000 must be filed via PTR within 45 days, but data is often stale by the time it goes public. |

| Legal duty established | 15 U.S.C. § 78u-1(g) creates a statutory duty of trust and confidence for members of Congress. |

| Enforcement gap | The maximum late-filing penalty is $200, and no member of Congress has been prosecuted under the Act. |

| Investor use case | PTR data is a transparency tool for pattern recognition, not direct evidence of illegal trading. |

The STOCK Act's intent versus its real-world impact

The STOCK Act was a genuine step forward. Before 2012, Congress operated in a legal vacuum on this issue. The law put insider trading rules in writing, created a public disclosure system, and gave prosecutors a statutory hook they did not have before. That matters.

But the gap between intent and execution is hard to ignore. A $200 fine for late disclosure is not a compliance mechanism. It is a formality. When the penalty for breaking a transparency rule costs less than a parking ticket, the rule does not change behavior. I have watched this pattern play out across financial regulation for years: disclosure without enforcement produces data, not accountability.

What the STOCK Act got right is the disclosure architecture. PTR filings, for all their limitations, created a public record that did not exist before. Journalists, watchdog groups, and data platforms now track congressional trades in ways that generate real political pressure. That pressure is arguably more effective than the law's formal penalties.

What it got wrong is the enforcement design. Delegating oversight to ethics committees that investigate their own members, while capping penalties at $200, was never going to produce serious deterrence. The reforms being debated in Congress, including outright bans on individual stock trading, reflect a recognition that disclosure alone is not enough.

For investors, the honest takeaway is this: the STOCK Act gives you data, not an edge. Use it to understand what lawmakers are doing with their portfolios. Treat it as one input in a broader research process. And recognize that the absence of prosecution does not mean the absence of problematic trading. It means the enforcement system was not built to catch it.

— Philip

Track congressional trades with Ai-stockscout

Congressional trade data is public. The challenge is parsing it fast enough to be useful.

Ai-stockscout pulls STOCK Act disclosure data alongside dark pool activity, insider filings, and social signals into one clean dashboard. You get real-time alerts when members of Congress file new PTRs, filtered by sector, ticker, or trade size. No manual searching through government portals. No waiting for a watchdog newsletter. Start free today at ai-stockscout.com and see congressional trades the moment they go public. The 3-day Pro trial costs nothing to start and cancels in one click.

FAQ

What does the STOCK Act do?

The STOCK Act prohibits members of Congress and federal employees from trading stocks based on material nonpublic information obtained through their official positions. It also requires public disclosure of qualifying trades over $1,000 within 45 days.

How long does Congress have to disclose a stock trade?

Covered transactions must be disclosed within 45 days of the trade date via a Periodic Transaction Report filed with the House or Senate disclosure system.

Has anyone been prosecuted under the STOCK Act?

No. No member of Congress has been prosecuted under the STOCK Act since it was signed into law in 2012, despite documented late filings and trades that raised conflict-of-interest concerns.

What is the penalty for violating the STOCK Act?

The primary enforcement mechanism is a maximum $200 fine for late disclosure filings, which is frequently waived. Criminal insider trading charges under general securities law are theoretically possible but have never been pursued.

Can investors use STOCK Act disclosures as trading signals?

PTR filings show transaction type and value ranges but omit exact prices, share counts, and trade rationale. They are useful for pattern recognition and accountability monitoring, not as direct evidence of insider trading or reliable buy/sell signals.